Provision For Bad Debts - Bad debts are amounts which are owed by a debtor and are not recovered, for example due to a company going bankrupt.

Provision For Bad Debts - Bad debts are amounts which are owed by a debtor and are not recovered, for example due to a company going bankrupt.. For example, if a company has issued invoices for a total of $1 million to its customers in a given month, and has a historical experience of 5% bad debts on its billings, it would. Bad debts as one of the confirmed losses a business needs to recognize in the period it happened; In that case, provision for bad debts would be an income statement account. 2.define accounts for reserve for bad debt here you need to assign bad debts expenses account and provision account. . the decrease of provisions for bad debts partially offset . the adverse effect of the above mentioned factors.

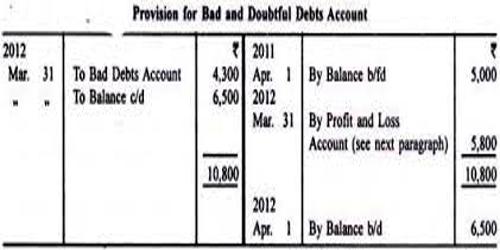

Next year, the actual amount of bad debts will be debited not to the profit and loss account but to the provision for bad and doubtful debts account which will then stand reduced. Dr bad debts cr provision for doubtful debts. Bad debts are amounts which are owed by a debtor and are not recovered, for example due to a company going bankrupt. . the decrease of provisions for bad debts partially offset . the adverse effect of the above mentioned factors. Balance sheet/statement of financial position extracts as at 31 december 20x7, 20x8 and 20x9.

Http Www Bookkeepers Org Uk Out Dlid 54337 from > bad debts and provision for doubtful debts. A bad debt provision is a reserve against the future recognition of certain accounts receivable as being uncollectible. The provision for bad and doubtful debts will appear in the balance sheet. . the decrease of provisions for bad debts partially offset . the adverse effect of the above mentioned factors. When the bad debt is recovered, there will be 2 entries: User end transactions system will automatically calculates the bad debts entry: Debit the provision doubtful debts account with the new provision and write is as balance c/d. For example, if a company has issued invoices for a total of $1 million to its customers in a given month, and has a historical experience of 5% bad debts on its billings, it would.

A bad debt provision is a reserve against the future recognition of certain accounts receivable as being uncollectible.

But since there is already an existing provision for$5,600 brought forward from the previous year, we need to create a further. 2.define accounts for reserve for bad debt here you need to assign bad debts expenses account and provision account. When an account is found to be uncollectible, then that account will be written off. Bad debt provision is reserve made to show the estimated percentage of the total bad and doubtful debts that needed to be written off in the next year and it is simply a loss because it is charged to profit & loss account of the company in the name of provision. Businesses usually create a provision for doubtful debt to provide for doubtful debts. Bad debts as one of the confirmed losses a business needs to recognize in the period it happened; Income and expenses from the accrual and release of bad debt provision are presented in the company's accounting reports on a net basis except for income from a release of the. Balance sheet/statement of financial position extracts as at 31 december 20x7, 20x8 and 20x9. Debit the provision doubtful debts account with the new provision and write is as balance c/d. Few reasons for debtors to not pay their debts on time may be; Bad debts dr provision cr. For example, if a company has issued invoices for a total of $1 million to its customers in a given month, and has a historical experience of 5% bad debts on its billings, it would. Accounting textbooks are more likely to use bad debts expense or uncollectible accounts.

Filing for bankruptcy, experiencing hardship due to losses, etc. There are two methods of reporting bad debt expense; Bad debts and provision for doubtful debts. Accounting textbooks are more likely to use bad debts expense or uncollectible accounts. For example, if a company has issued invoices for a total of $1 million to its customers in a given month, and has a historical experience of 5% bad debts on its billings, it would.

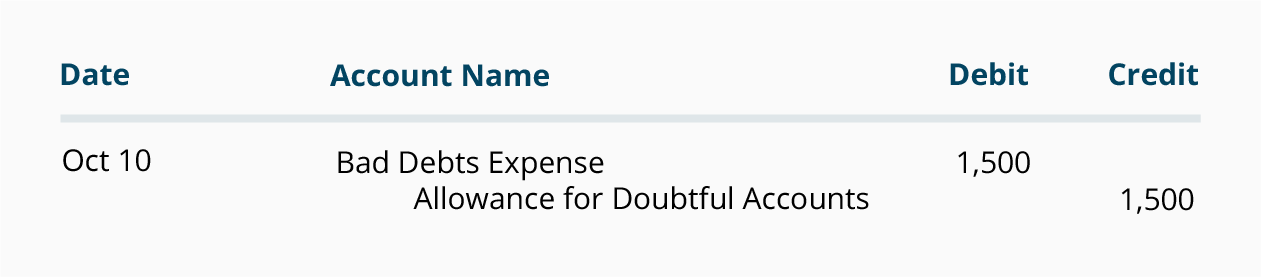

Provision For Bad And Doubtful Debts Qs Study from qsstudy.com Provision for bad and doubtful debts year end p&l a/c dr to doubtful debts a/c ( this is a closing entry) in the balance sheet, the provision for bad and doubtful debts a/c is shown as a deduction from sundry debtor's a/c this satisfies the matching principle and the concept of prudence. Filing for bankruptcy, experiencing hardship due to losses, etc. User end transactions system will automatically calculates the bad debts entry: Businesses usually create a provision for doubtful debt to provide for doubtful debts. In this situation you enter a provision for an amount which you think will go bad, so your accounts only show an amount which you are likely to. (2) specific provision for doubtful debts: In conclusion, provision for doubtful debts and provision for bad debts are used interchangeably in several textbooks, however they usually mean the as for the above question, both the bad debts and provision for bad debts are debited to profit and loss account. When the bad debt is recovered, there will be 2 entries:

Fyi i cover bad debts and provision for bad debts in a lot more detail in my accounting books, with full lessons, examples and exercises.

The provision for bad and doubtful debts will appear in the balance sheet. User end transactions system will automatically calculates the bad debts entry: For example, if a company has issued invoices for a total of $1 million to its customers in a given month, and has a historical experience of 5% bad debts on its billings, it would. Debit the provision doubtful debts account with the new provision and write is as balance c/d. On december 17, 2010, the fasb took the uncommon step of issuing for comment a revised ed, presentation and disclosure of net revenue, provision for bad debts, and the allowance for doubtful accounts, which reflects the. Balance sheet/statement of financial position extracts as at 31 december 20x7, 20x8 and 20x9. Dr bad debts cr provision for doubtful debts. There are two methods of reporting bad debt expense; In conclusion, provision for doubtful debts and provision for bad debts are used interchangeably in several textbooks, however they usually mean the as for the above question, both the bad debts and provision for bad debts are debited to profit and loss account. A bad debt provision is a reserve against the future recognition of certain accounts receivable as being uncollectible. The provision for doubtful debts is an estimated amount of bad debts that are likely to arise from the accounts receivable that have been given but not yet such provision is provided for, under accrual basis accounting, so that an expense is usually recognized for probable bad debts as soon as. . the decrease of provisions for bad debts partially offset . the adverse effect of the above mentioned factors. In that case, provision for bad debts would be an income statement account.

Now we will look at an example provision for doubtful debts accounts for each of the three years. Debit the provision doubtful debts account with the new provision and write is as balance c/d. And the doubtful debts ie an expected future loss that needs to be provided for in order to report the financials in a. Reverse the bad debts provision and 2. (2) specific provision for doubtful debts:

Writing Off An Account Under The Allowance Method Accountingcoach from www.accountingcoach.com Bad debts dr provision cr. Provision for bad and doubtful debts year end p&l a/c dr to doubtful debts a/c ( this is a closing entry) in the balance sheet, the provision for bad and doubtful debts a/c is shown as a deduction from sundry debtor's a/c this satisfies the matching principle and the concept of prudence. Bad debt provision calculation can be done in two ways. User end transactions system will automatically calculates the bad debts entry: Bad debts actually written off in the year are $5,420 debtors at the end of the year are $350,000 provisions for bad debts at 2% of this amount would come to $7,000. For example, if a company has issued invoices for a total of $1 million to its customers in a given month, and has a historical experience of 5% bad debts on its billings, it would. Best, michael celender founder of accounting basics for students. We debit the bad debt expense account, we don't debit sales to remove the sale.

User end transactions system will automatically calculates the bad debts entry:

Bad debts as one of the confirmed losses a business needs to recognize in the period it happened; We debit the bad debt expense account, we don't debit sales to remove the sale. Bad debts are amounts which are owed by a debtor and are not recovered, for example due to a company going bankrupt. And the doubtful debts ie an expected future loss that needs to be provided for in order to report the financials in a. The provision for doubtful debts is an estimated amount of bad debts that are likely to arise from the accounts receivable that have been given but not yet such provision is provided for, under accrual basis accounting, so that an expense is usually recognized for probable bad debts as soon as. When the bad debt is recovered, there will be 2 entries: For example, if a company has issued invoices for a total of $1 million to its customers in a given month, and has a historical experience of 5% bad debts on its billings, it would. The word specific means that there is clear documentary evidence like litigation and other findings that show that a particular trade receivable might turn bad (irrecoverable). Filing for bankruptcy, experiencing hardship due to losses, etc. We have looked at bad debts, provision for doubtful debts and bad debts recovered. In that case, provision for bad debts would be an income statement account. If so, the account provision for bad debts is a contra asset account (an asset account with a credit balance). There are two methods of reporting bad debt expense;

Related : Provision For Bad Debts - Bad debts are amounts which are owed by a debtor and are not recovered, for example due to a company going bankrupt..